Comments on the articles of Model 1A of the Intergovernmental Agreement to Improve Tax Compliance and to Implement FATCA

On 18 March 2010 the US enacted the Foreign Account Tax Compliance Provisions known as FATCA. FATCA requires financial institutions outside the US to report information on US account holders directly to the US tax authorities. If financial institutions fail to report the required information then 30% US tax would be withheld on all US payments to them. The governments of France, Germany, Italy, Spain and the United Kingdom (the G5) approached the US setting out the concerns of their financial institutions regarding the operation of FATCA and specifically how, due to legal constraints, they would not be able to deliver the information in the manner designed by the US legislation. On 8 February 2012, the G5 and the US issued a Joint Statement setting out agreement to explore an intergovernmental approach to implementing FATCA. Following further negotiations, on 26 July 2012 the G5 and US issued a further Joint Statement announcing the publication of the «Model Intergovernmental Agreement to Improve Tax Compliance and to Implement FATCA» (the Model IGA). Since then, Model IGA is becoming the legal way through which FATCA is going to be implemented in the vast majority of developed and emergent countries.

FATCA is the acronym for the Foreign Account Tax Compliance Act, a law approved by the US Internal Revenue Service (IRS) and the US Treasury Department on 18 March 2010 to promote the tax transparency and encourage compliance by US persons with their tax obligations.

FATCA requires financial institutions around the world to identify those clients who are United State persons who have – among others – financial accounts in foreign countries that must be reported annually to the US tax authorities. To ensure compliance with FATCA, a 30% withholding will be applied to certain payments made to entities and people who do not comply with this regulation.

Due to the extraterritorial scope of this law, the United States has adopted an intergovernmental approach that consists of entering into bilateral agreements (Intergovernmental Agreement or IGA) with certain countries. Under these bilateral agreements, FATCA regulations are transposed into the internal laws of the signatory country in order to facilitate the practical enforcement of FATCA obligations.

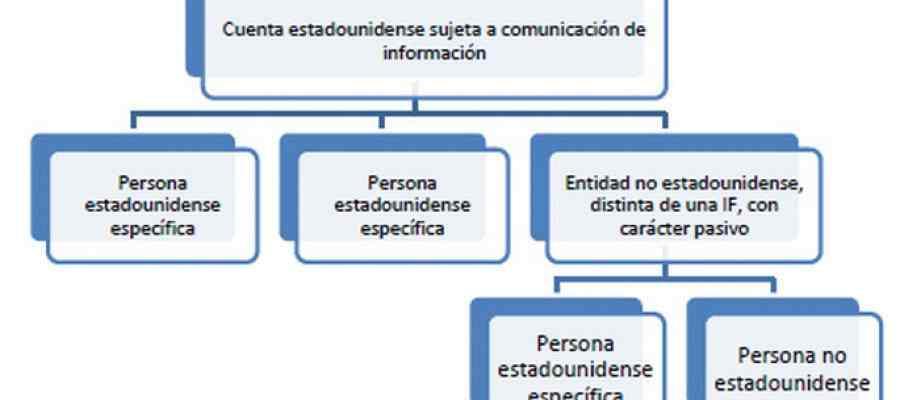

In general, the obligations imposed by FATCA are as follows:

- Registration on the IRS website set up for this purpose.

- Identification of any US Person who has an account with the bank and falls into any of the following categories:

- Citizens or legal residents of the United States. Not only US persons who reside in the US but also those who possess American citizenship, regardless of where they live, are bound by US tax laws.

- Companies incorporated in the United States or owned by one or more US Persons who exercise control of the company.

- The following information on the financial accounts of clients identified as US Persons must be reported to the IRS annually:

- Personal information: name, address and US tax identification number (US TIN).

- Financial information such as the account number, the year-end balance, closed accounts, final balances and income earned on the account.

Financial accounts are understood as deposit, custody, and equity accounts and some insurance policies.

- The withholding rules even apply to financial institutions that have not signed a FATCA agreement and clients with fiscal obligations in the United States who do not provide their information willingly or do not consent to report their information to the IRS (recalcitrant clients).

I had a really urgent problem in the middle of the summer that I needed to get fixed. I tried contacting a bunch of agencies but they were either unavailable, slow, had terrible service or were crazy expensive (one company quoted me 1000€!). Josep replied to me within 10 minutes and managed to submit my forms on the deadline and all for a great price. He saved my life - 100% recommend!